Don’t Expect to See the Yield Curve Invert Before a Recession dated 04/13/18

While the last six U.S. recessions (back to ’69) were preceded by yield curve inversions, the six before that (back to 1937) were not. This is because these were different type of recessions: the recent recessions before 2008 were ‘inventory-cycle’ recessions, not ‘balance-sheet’ recessions.

Because 2008 was once-in-a-generation, it has depressed long-term growth rates because of the need of ongoing de-leveraging, which in turn forces the central banks to keep the short-term rates low, and this continues for a couple of decades or so. The fragile state of the economy during these cycles (post-balance sheet recessions) prevents the central bank from getting a normal rate rise cycle in (i.e. raising the short-term rates).

The Secular Trend In Interest Rates Remains Lower dated 11/15/16

According to Larry Summers, after 5 years of expansion, the chances of a recession increases by 20% every year.

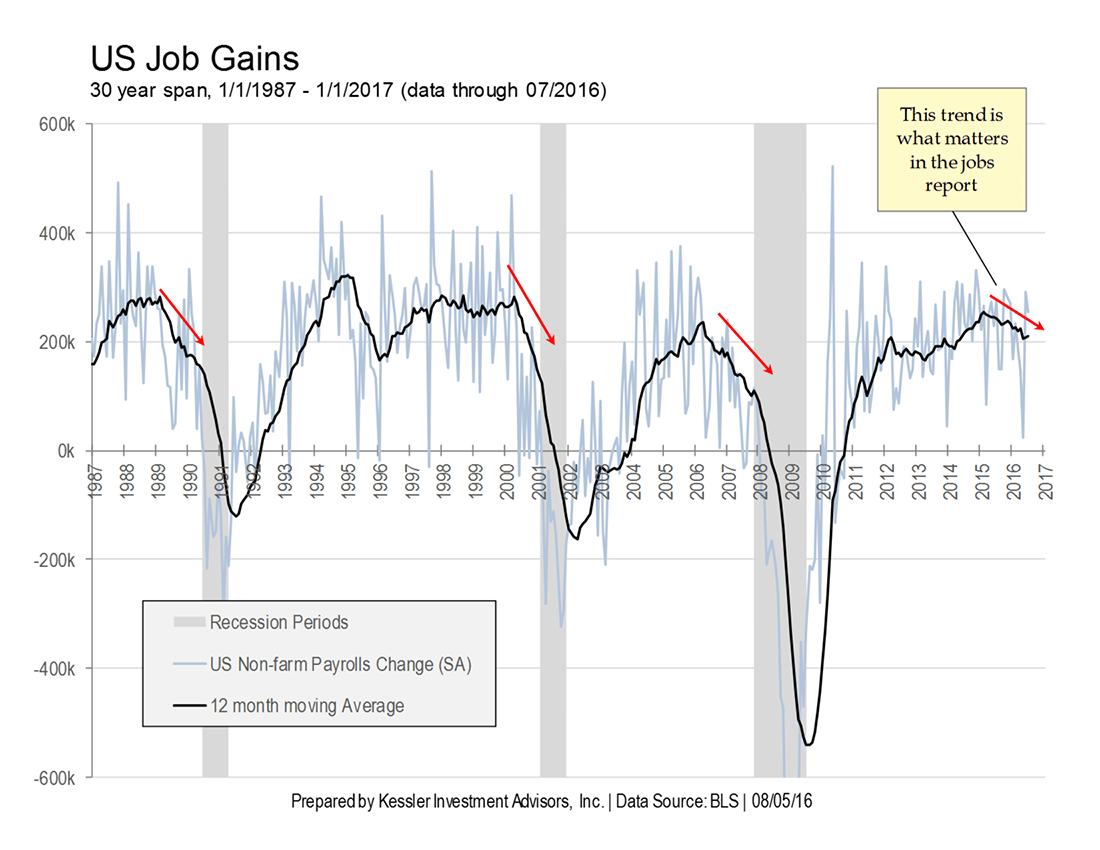

Don’t Be Fooled dated 08/05/16

The article shows how the recent job growth is masking a somewhat deteriorating job market (once you adjust for the seasonal adjustment and the job trend).

The article shows this image (original image at http://www.kesslercompanies.com/content/dont-be-fooled)

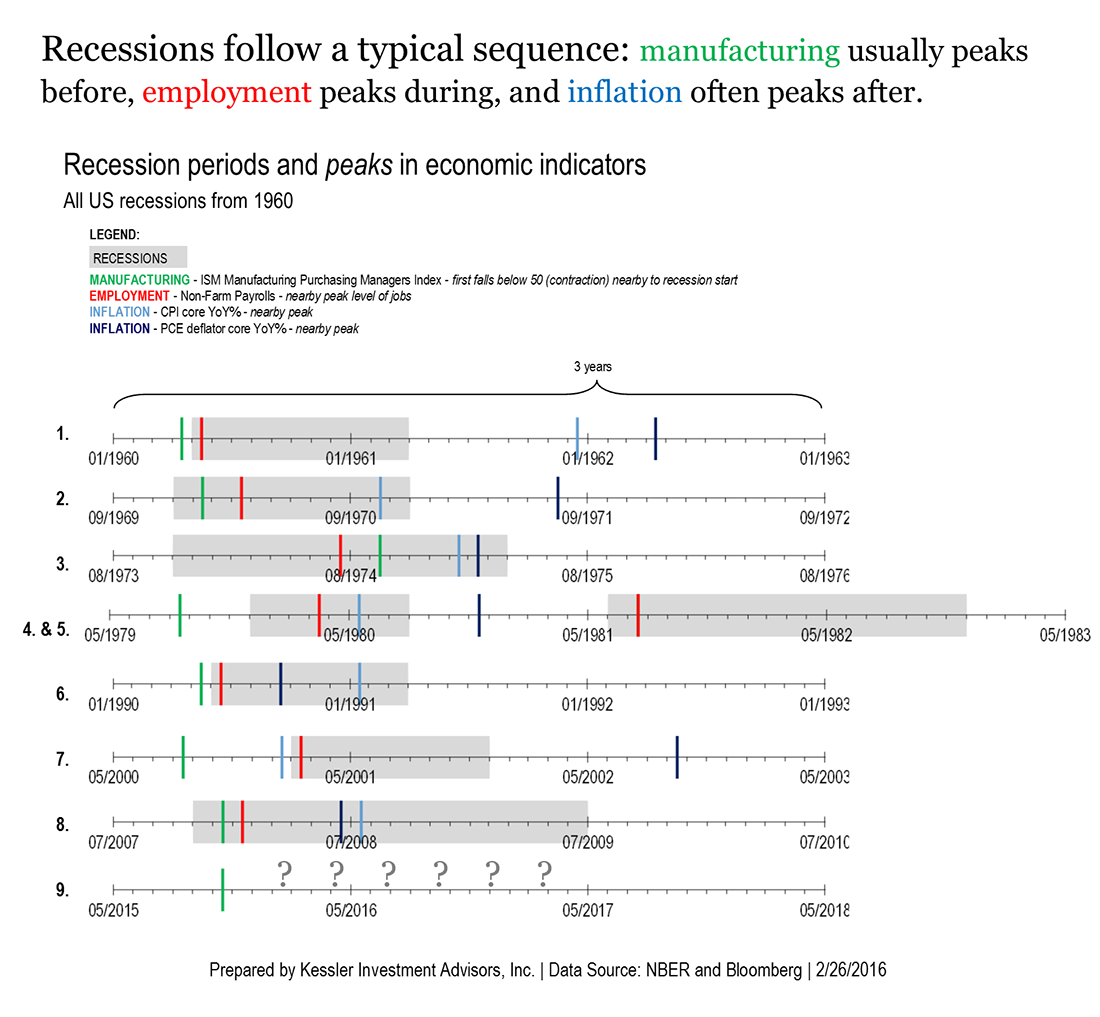

Mind the Business Cycle, Part 2 dated 02/26/16

The article states: “Counter-intuitively, the recent increases in core inflation are normal in the sequence of how a recession evolves. The typical business-cycle sequence is that the manufacturing sector weakens first, then employment and consumer spending, and lastly, inflation. In fact, it is often not until the recession is over that inflation begins to come down. Inflation is the longest lagging indicator.” This is important because inflation is cited as hawks to raise interest rates as the economy is crumbling beneath.

The article also shows this beautiful image (original image at http://www.kesslercompanies.com/content/mind-business-cycle-part-2)